Eratat is a counter listed on SGX. Previously, I have expressed concerns over its business model and its obscene amount of trade receivables.

Subsequently, Eratat reduced its trade receivables, not by collecting back the cash, but by providing something called a renovation subsidy. Which sounds nice, but still means ultimately, the cash didn't get to them.

It has been quite a while since I studied their statements. There were some people who were pointing to the SIAS research as the "authority", and expressed their confidence in this counter because SIAS said so, especially after I have expressed concerns over it. Certain things that are red herrings in my opinion are then brushed away. :(

I dug out the past reports of SIAS research on Eratat. Each and every one of the reports mentioned Increased Exposure, even though the estimated Intrinsic Value calculated by the analyst went to S$0.27.

Interestingly, the highest price the counter has ever went to was S$0.28.

Checking the history reports by SIAS (no offence meant to any organisation),

23rd Sep 2010 Intrinsic Value S$0.320 Title: New Business Shows Great Promise

06th Oct 2010 Intrinsic Value S$0.320 Title: Running a Tight Ship

04th Nov 2010 Intrinsic Value S$0.450 Title: An Exciting Set of Results - 108% Growth

01st Mar 2011 Intrinsic Value S$0.480 Title: Time for value to be recognized.

05th Apr 2011 Intrinsic Value S$0.480 Title: Do you want to miss this ride?

07th Apr 2011 Intrinsic Value S$0.420 Title: Fast and Furious

11th May 2011 Intrinsic Value S$0.430 Title: Yet Another Exciting Set of Results

05th Aug 2011 Intrinsic Value S$0.325 Title: Strong Growth Revisited

06th Sep 2011 Intrinsic Value S$0.325 Title: China’s Gateway to European Fashion

08th Nov 2011 Intrinsic Value S$0.325 Title: Climbing the Brand Value Ladder

23rd Feb 2012 Intrinsic Value S$0.325 Title: Accumulate on Overreaction to Results

12th Apr 2012 Intrinsic Value S$0.325 Title: Treading New Ground in Trade Show

14th Aug 2012 Intrinsic Value S$0.240 Title: Focus Shifting to Distribution Expansion

05th Nov 2012 Intrinsic Value S$0.240 Title: 3Q Results Showed Improvement Over 1H

26th Feb 2013 Intrinsic Value S$0.270 Title: 4Q Results Back to Par

02th May 2013 Intrinsic Value S$0.270 Title: Higher Volume, Higher Prices for Apparel

13th May 2013 Intrinsic Value S$0.270 Title: Preparing for the Next Lap of Growth

In all reports, the analyst maintained increase exposure. And in all the reports, the intrinsic value is higher than the share price.

Clearly, it can be seen that unless an investor bought in at the ultimate low, he/she will most likely be facing a big paper loss following the research reports. Well... The "investor" may make a profit another few years down the road. The question is then, how many years does that few years mean?

Research reports protect themselves by

"As of the date of this report, the analyst and his immediate family may own or have positions in any securities mentioned herein or any securities related thereto and may from time to time add or dispose of or may be materially interested in any such securities.

...

...

The use of this material does not absolve you of your responsibility for your own investment decisions. We accept no liability for any direct or indirect loss arising from the use of this research material. We, our associates, directors and/or employees may have an interest in the securities and/or companies mentioned herein."

The analyst and organisation are protected by their disclaimers, but your money isn't.

Neither does any of my blog posts constitute any solicitation of an offer to buy or sell any securities. ")

Moral of the story: Do your own thorough homework.

Stocks, Personal Finance, Personal Development,

Wealth, Income, Trading, Investing, Business

test4

Friday, May 17, 2013

Friday, May 10, 2013

Are you planning on starting a new business?

But why??!

This post was inspired by the number of people whom I have talked to and aspire to start their own businesses for a few common reasons.

Back in 2012, when I left my job to do full-time tuition and run a tuition centre as a business, I was thinking. Was I foolish to do so? Probably. My portfolio would have been much bigger than now had I continued as an employee while doing tuition part time, although I would have been much more tired with much less free time.

Since then, while I have not regretted the move (yet), my income certainly hasn't seen a phenomenal growth. I was fortunate to have built a sufficient war chest enough to last me for quite a few years, and fortunate not to be making losses (yet).

The learning curve so far was steep, very very steep. I know I have learned much more over the past 8 months than I did over the 4 years I was employed. I have learned what is meant by marketing, advertising, branding, as well as the different government grants and taxes, the different company structures, more about profits and losses, etc. In addition, I have met up with many people over different industries, talked to many friends who have their own aspirations, etc.

It is interesting that a number of people out there are a little dissatisfied about their jobs. Yet most of them stayed at the same job for the same few reasons

1) "I need the money."

2) "I don't know what else I can do."

3) "I want to start a business, but I don't know what business I can start."

4) "If I failed, I don't think I will be able to get employment again at this age."

and probably more I can't remember for now.

To me, the reasons can be broadly classified into one category, Fear.

The fear of change, and the fear of failure.

In my previous company, my superior used to tell me (and quite frequently), "don't be too creative in your approach, just do the necessary things to complete it. You still have a long future ahead in this company." This happens in most of the times I suggested certain changes, which probably are too radical I supposed, to be fair.

Don't get me wrong, there's nothing wrong at all playing safe all the time, and there's nothing wrong staying employed. But to me, if one wants to start a business to take on the stiff competition in the unsheltered outside world, one needs to step out of the box and try different things. It is not about playing safe, it is about daring to change, daring to fail, and daring to pick up from failures.

For the unsuspecting who are planning on starting a new business, what are your reasons?

Let's get a reality check on the common reasons.

“I’m working so hard at my job and being so stressed all the time.”

But hey, doing business is more hard work than ever before! Your business system isn't ready, and your responsibilities are much more! Any medical leave or vacation leave you take in the initial stages may cost you your business.

My friends usually raised their eyebrows when I told them I'm actually working harder while earning less now. Well...

"I need a second income stream."

Then why run a business? Why not just take on another part-time job, like driving a taxi, etc? Expenses usually comes before revenues, and the expenses could kill you before the business turns into an income stream.

Business building and branding takes time, lots of it. And the amount of time needed could be quite demoralizing. Just imagine weeks and months with minimal business.

“I hate my boss, and dislike being an employee.”

I realised I have more bosses now. My students, their parents, and even my partner and my tutors are all my bosses.

In a way, I have to meet objectives of many more people than before.

“A business will make me rich.”

In a way, I am probably a living example at the moment that starting out by myself earns me less than if I was a working professional. Certainly, there are examples out there where running a business earns the entrepreneur more than what he/she would earn if he/she remained employed, but I guess for the majority, it may not be the case.

As of now, I have my fair share of frustrations, of failures and of headaches of my first attempt to do a tuition business. The business aspect of tuition is addictive, but results are seldom immediate. An advertisement once out, seldom bring an immediate response. The same goes for any other marketing or advertising activities. Branding, recognition, takes time to build.

For everyone who have an aspiration to start a business, I hope I have not discouraged you. Because if you get discouraged just by a blog post, you are probably not suited to start one.

* What makes me continue in this is the addiction of running a business (or more than 1). To me, it feels like playing chess. I was a chess player during my student days, and honestly I was addicted. Every move I make in an attempt to advance my business position is like making a move on the chessboard. The difference is this chess game is for the game of life, and my opponents numbered more than one.

This post was inspired by the number of people whom I have talked to and aspire to start their own businesses for a few common reasons.

Back in 2012, when I left my job to do full-time tuition and run a tuition centre as a business, I was thinking. Was I foolish to do so? Probably. My portfolio would have been much bigger than now had I continued as an employee while doing tuition part time, although I would have been much more tired with much less free time.

Since then, while I have not regretted the move (yet), my income certainly hasn't seen a phenomenal growth. I was fortunate to have built a sufficient war chest enough to last me for quite a few years, and fortunate not to be making losses (yet).

The learning curve so far was steep, very very steep. I know I have learned much more over the past 8 months than I did over the 4 years I was employed. I have learned what is meant by marketing, advertising, branding, as well as the different government grants and taxes, the different company structures, more about profits and losses, etc. In addition, I have met up with many people over different industries, talked to many friends who have their own aspirations, etc.

It is interesting that a number of people out there are a little dissatisfied about their jobs. Yet most of them stayed at the same job for the same few reasons

1) "I need the money."

2) "I don't know what else I can do."

3) "I want to start a business, but I don't know what business I can start."

4) "If I failed, I don't think I will be able to get employment again at this age."

and probably more I can't remember for now.

To me, the reasons can be broadly classified into one category, Fear.

The fear of change, and the fear of failure.

In my previous company, my superior used to tell me (and quite frequently), "don't be too creative in your approach, just do the necessary things to complete it. You still have a long future ahead in this company." This happens in most of the times I suggested certain changes, which probably are too radical I supposed, to be fair.

Don't get me wrong, there's nothing wrong at all playing safe all the time, and there's nothing wrong staying employed. But to me, if one wants to start a business to take on the stiff competition in the unsheltered outside world, one needs to step out of the box and try different things. It is not about playing safe, it is about daring to change, daring to fail, and daring to pick up from failures.

For the unsuspecting who are planning on starting a new business, what are your reasons?

Let's get a reality check on the common reasons.

“I’m working so hard at my job and being so stressed all the time.”

But hey, doing business is more hard work than ever before! Your business system isn't ready, and your responsibilities are much more! Any medical leave or vacation leave you take in the initial stages may cost you your business.

My friends usually raised their eyebrows when I told them I'm actually working harder while earning less now. Well...

"I need a second income stream."

Then why run a business? Why not just take on another part-time job, like driving a taxi, etc? Expenses usually comes before revenues, and the expenses could kill you before the business turns into an income stream.

Business building and branding takes time, lots of it. And the amount of time needed could be quite demoralizing. Just imagine weeks and months with minimal business.

“I hate my boss, and dislike being an employee.”

I realised I have more bosses now. My students, their parents, and even my partner and my tutors are all my bosses.

In a way, I have to meet objectives of many more people than before.

“A business will make me rich.”

In a way, I am probably a living example at the moment that starting out by myself earns me less than if I was a working professional. Certainly, there are examples out there where running a business earns the entrepreneur more than what he/she would earn if he/she remained employed, but I guess for the majority, it may not be the case.

As of now, I have my fair share of frustrations, of failures and of headaches of my first attempt to do a tuition business. The business aspect of tuition is addictive, but results are seldom immediate. An advertisement once out, seldom bring an immediate response. The same goes for any other marketing or advertising activities. Branding, recognition, takes time to build.

For everyone who have an aspiration to start a business, I hope I have not discouraged you. Because if you get discouraged just by a blog post, you are probably not suited to start one.

* What makes me continue in this is the addiction of running a business (or more than 1). To me, it feels like playing chess. I was a chess player during my student days, and honestly I was addicted. Every move I make in an attempt to advance my business position is like making a move on the chessboard. The difference is this chess game is for the game of life, and my opponents numbered more than one.

Thursday, May 9, 2013

US Markets hitting new highs!

*** Note: This post is of a very simplified calculation. There's nothing professional in it. ***

The numbers are appearing to break new highs. USA has broken it's high of 14198 in 2007 while STI appears to be languishing far below the 2007 high of 3906.

But is it really due to nominal value or currency value?

I shall make a simple comparison using USD to SGD as a simple consideration.

Adjusting for Currency Value + inflation

********************************************************************

Year 2007:

1 USD = 1.55 SGD

Dow Jones hit a high of 14198

Year 2009:

1 USD = 1.5 SGD

Dow Jones hit a low of 6469

Year 2013

1 USD = 1.23 SGD

Supposed value of SGD (simplified assumption) remains a constant,

14198 will work out to be 17892 (14198 / 1.23 * 1.55)

6469 will work out to be 7889 (14198 / 1.23 * 1.5)

Adjusting for average inflation rate of 2.0% for the USA from 2007 to 2013,

17892 will turn to 20149 today

7889 will turn to 8539 today

There is difference of 11610. Given the Dow Jones close is 15105, a difference of 6566 from the low.

The retracement percentage is roughly 56.6%

And if we assume the SGD stays at a constant value throughout.

With a high of 3906 in 2007 and a low of 1455 in 2009 (numbers from daily values of STI from Yahoo Finance)

Adjusting for average inflation rate of 3.5% for Singapore from 2007 to 2013,

3906 will turn to 4801 today

1455 will turn to 1670 today

There is difference of 3132. Given the STI is about 3430, a difference of 1760 from the low.

The retracement percentage is roughly 56.2%

In other words, nominalizing all to SGD and country inflation rate actually shows that the retracement percentages are very close (56.5% vs 56.2%).

So while the numbers in Dow looks to be breaking new highs, it is in my opinion a credit driven rally, made possible by the devaluation of the USD. In other words, valuations of stocks in USD are higher because valuations of USD has dropped significantly.

Just some two cents of thoughts, with plenty of simplifications.

The numbers are appearing to break new highs. USA has broken it's high of 14198 in 2007 while STI appears to be languishing far below the 2007 high of 3906.

But is it really due to nominal value or currency value?

I shall make a simple comparison using USD to SGD as a simple consideration.

Adjusting for Currency Value + inflation

********************************************************************

Year 2007:

1 USD = 1.55 SGD

Dow Jones hit a high of 14198

Year 2009:

1 USD = 1.5 SGD

Dow Jones hit a low of 6469

Year 2013

1 USD = 1.23 SGD

Supposed value of SGD (simplified assumption) remains a constant,

14198 will work out to be 17892 (14198 / 1.23 * 1.55)

6469 will work out to be 7889 (14198 / 1.23 * 1.5)

Adjusting for average inflation rate of 2.0% for the USA from 2007 to 2013,

17892 will turn to 20149 today

7889 will turn to 8539 today

There is difference of 11610. Given the Dow Jones close is 15105, a difference of 6566 from the low.

The retracement percentage is roughly 56.6%

And if we assume the SGD stays at a constant value throughout.

With a high of 3906 in 2007 and a low of 1455 in 2009 (numbers from daily values of STI from Yahoo Finance)

Adjusting for average inflation rate of 3.5% for Singapore from 2007 to 2013,

3906 will turn to 4801 today

1455 will turn to 1670 today

There is difference of 3132. Given the STI is about 3430, a difference of 1760 from the low.

The retracement percentage is roughly 56.2%

In other words, nominalizing all to SGD and country inflation rate actually shows that the retracement percentages are very close (56.5% vs 56.2%).

So while the numbers in Dow looks to be breaking new highs, it is in my opinion a credit driven rally, made possible by the devaluation of the USD. In other words, valuations of stocks in USD are higher because valuations of USD has dropped significantly.

Just some two cents of thoughts, with plenty of simplifications.

Tuesday, May 7, 2013

Growing your business with PIC

PIC stands for Productivity and Innovation Credit. It took me the past few months to really study through all the documents on the IRAS website, to ponder, think through, calculate, before I make the application.

In short, it is a very powerful grant by the government to grow your business's productivity.

It can be applied in 6 areas

1) Acquisition and leasing of PIC Information Technology (IT) and Automation Equipment;

2) Training of employees;

3) Acquisition and In-licensing of Intellectual Property Rights;

4) Registration of patents, trademarks, designs and plant varieties;

5) Research and development activities; and

6) Design projects approved by DesignSingapore Council.

From a business perspective, it makes sense to spend time studying this, and to invest wisely into improving the business productivity with this grant.

In short, it is a very powerful grant by the government to grow your business's productivity.

It can be applied in 6 areas

1) Acquisition and leasing of PIC Information Technology (IT) and Automation Equipment;

2) Training of employees;

3) Acquisition and In-licensing of Intellectual Property Rights;

4) Registration of patents, trademarks, designs and plant varieties;

5) Research and development activities; and

6) Design projects approved by DesignSingapore Council.

Basically, I think (1) and (4) applies to most businesses, especially (1).

A computer, a photocopier, modems, hard disk storages, display TVs, all count towards (1).

For businesses with big profits, you probably don't even need to read this post. Just go ahead with the 400% tax deductions. For small businesses who don't make much profits, the 60% cash payout option makes more sense.

In layman terms, 60% cash payout means IRAS pays 60% of the expenditure made in the 6 qualifying activities. That means for every $1000 invested into (1), IRAS pays you $600, subjected to a maximum investment of $100k per year per activity. Well, my really small tuition business will not exceed that definitely.

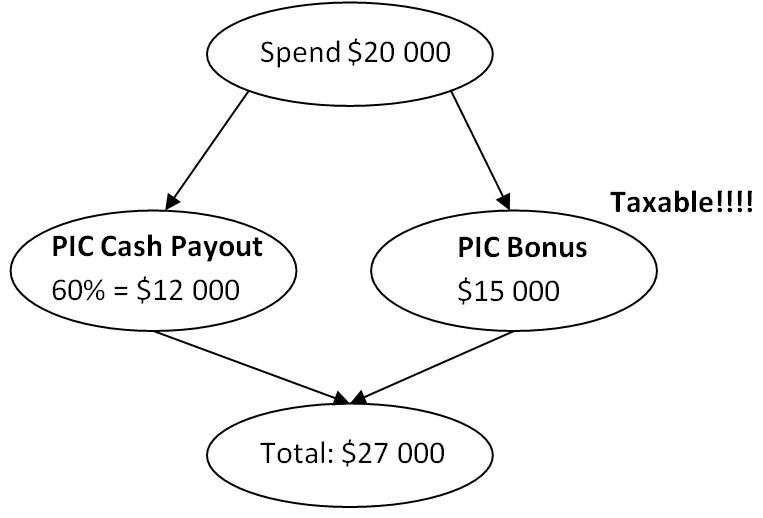

As of budget 2013, a new scheme called PIC Bonus is implemented. Well, luckily I waited till past this budget before I made any decision. In short, IRAS gives dollar for dollar on the expenditure, subjected to a cap of $15k.

A graphical scheme is displayed below.

It looks nice on the surface, but of course, there is a catch to this.

1) The PIC Bonus is taxable! So the $15k will be considered part of revenue!

However, the PIC Cash Payout is not considered part of revenue. Additionally, the purchase of the equipments cannot be counted towards capital allowance.

2) Contributions to 3 local employees' CPF needed in the last month of the quarter. Owners, shareholders and directors of the business is not included.

The criteria is pretty comprehensive . More details can be found here:

Part-time and full-time employees are both applicable to the 3 local employees criteria, provided all are Singaporeans or Singapore PRs.

From a business perspective, it makes sense to spend time studying this, and to invest wisely into improving the business productivity with this grant.

Monday, May 6, 2013

Taking a little profit off the table

Over the past week, I have disposed of Singtel and SingPost.

The reason for the disposal are

1) Singtel, sold at $3.92, is quite near it's past recent high of $4.17

2) Singpost, sold at $1.29, is near it's past recent high of $1.30

There's a time for buying, and there's a time for selling. While the market may look to be on a bullish run, there's always a time the music will end.

Just don't get caught naked when the tide runs out ;)

While the music is still on, and the interest rates still low, I will be looking to sell a few more counters which I don't really like the business or the dividend yields, but bought because I think the prices were too low.

The counters are

1) CitySpring. I'm uncomfortable about its high debt, although the dividend yield is moderately acceptable.

2) Capitaland. The business of this volatile stock is probably ok, but its dividend yield is way too low, and hence the returns aren't that great. I have this counter since March 2009 at a very low price, but I might consider offloading all.

3) CapitalMallAsia. Same as point (2)

4) GLP. The business is probably ok, but I think it is getting a bit too pricey. I don't have a calculation of its value; it is more of a gut feel that $3 may be a sell.

5) Silverlake. The business is really great. But the price has gone really high too. I will have to evaluate the counter again, something which I have not done for a long time. With a 112% gain on top of the 5% annual yield, I guess I do have some leeway to play around :)

6) Cosco. My first stock bought at $2.67. Am considering to cut loss on this, buoyant by massive gains in other counters. A stock bought with zero analysis except hearsay from my sis. :x

7) Aztech. Probably a wrong FA purchase.

8) Hor Kew. Another wrong purchase.

9) SPH. Well, I like the business, but I'm unsure if the counter is worth $4.40.

10) Starhub. One of my biggest gains in my portfolio, apart from AIMSAMPIREIT. With a 147% gain and a annual 10.5% dividend yield, I couldn't be happier :) But at around $4.70? Is it too high for such a counter? I might sell some such that my remaining counters cost $0.

Not in a rush to sell, but I'm starting to monitor again. I will probably sell some REITs soon too, just not yet...

All in all, the amount I'm eyeing to sell is about $80k and up. The cash will probably be re-invested into a second business venture, as well as invested into my wedding next year :)

My dividend yield will probably be adversely affected, but in a way, with the amount of paper gain, I could probably treat it as taking my dividends for 10 years early. Surely 10 years would be a sufficient time frame to see the next bear market.

As an afterthought after HM Shak's comment below:

Using Fibonacci Retracement on the STI,

In any case, if we take 1513 as the reference low and 3857 as the reference high from Yahoo Finance, the 76.8% retracement is 3313 and the 78.6% retracement is 3355. If we take into account the intra-day fluctuations (which I didn't bother to dig out), the values could be higher, and 3400 is about right.

This was my plan since 2011:

http://wealthbuch.blogspot.sg/2011/02/personal-updates.html

The reason for the disposal are

1) Singtel, sold at $3.92, is quite near it's past recent high of $4.17

2) Singpost, sold at $1.29, is near it's past recent high of $1.30

There's a time for buying, and there's a time for selling. While the market may look to be on a bullish run, there's always a time the music will end.

Just don't get caught naked when the tide runs out ;)

While the music is still on, and the interest rates still low, I will be looking to sell a few more counters which I don't really like the business or the dividend yields, but bought because I think the prices were too low.

The counters are

1) CitySpring. I'm uncomfortable about its high debt, although the dividend yield is moderately acceptable.

2) Capitaland. The business of this volatile stock is probably ok, but its dividend yield is way too low, and hence the returns aren't that great. I have this counter since March 2009 at a very low price, but I might consider offloading all.

3) CapitalMallAsia. Same as point (2)

4) GLP. The business is probably ok, but I think it is getting a bit too pricey. I don't have a calculation of its value; it is more of a gut feel that $3 may be a sell.

5) Silverlake. The business is really great. But the price has gone really high too. I will have to evaluate the counter again, something which I have not done for a long time. With a 112% gain on top of the 5% annual yield, I guess I do have some leeway to play around :)

6) Cosco. My first stock bought at $2.67. Am considering to cut loss on this, buoyant by massive gains in other counters. A stock bought with zero analysis except hearsay from my sis. :x

7) Aztech. Probably a wrong FA purchase.

8) Hor Kew. Another wrong purchase.

9) SPH. Well, I like the business, but I'm unsure if the counter is worth $4.40.

10) Starhub. One of my biggest gains in my portfolio, apart from AIMSAMPIREIT. With a 147% gain and a annual 10.5% dividend yield, I couldn't be happier :) But at around $4.70? Is it too high for such a counter? I might sell some such that my remaining counters cost $0.

Not in a rush to sell, but I'm starting to monitor again. I will probably sell some REITs soon too, just not yet...

All in all, the amount I'm eyeing to sell is about $80k and up. The cash will probably be re-invested into a second business venture, as well as invested into my wedding next year :)

My dividend yield will probably be adversely affected, but in a way, with the amount of paper gain, I could probably treat it as taking my dividends for 10 years early. Surely 10 years would be a sufficient time frame to see the next bear market.

As an afterthought after HM Shak's comment below:

Using Fibonacci Retracement on the STI,

In any case, if we take 1513 as the reference low and 3857 as the reference high from Yahoo Finance, the 76.8% retracement is 3313 and the 78.6% retracement is 3355. If we take into account the intra-day fluctuations (which I didn't bother to dig out), the values could be higher, and 3400 is about right.

This was my plan since 2011:

http://wealthbuch.blogspot.sg/2011/02/personal-updates.html

Subscribe to:

Posts (Atom)